.gif)

|

Signature Sponsor

March 7, 2017 - With 2016 being a year of rock bottom-of-cycle prices, many expected it to also be a good year for mining mergers and acquisitions (M&A).

But while the number of deals made last year increased by a third from the year prior, to 477 deals in 2016, it's the low value of the M&A that stands out in EY's latest report, "Mergers, acquisitions and capital raisings in mining and metals – 2016 trends, 2017 outlook."

Copper was the commodity of most interest, comprising three of the top 10 deals, by value.

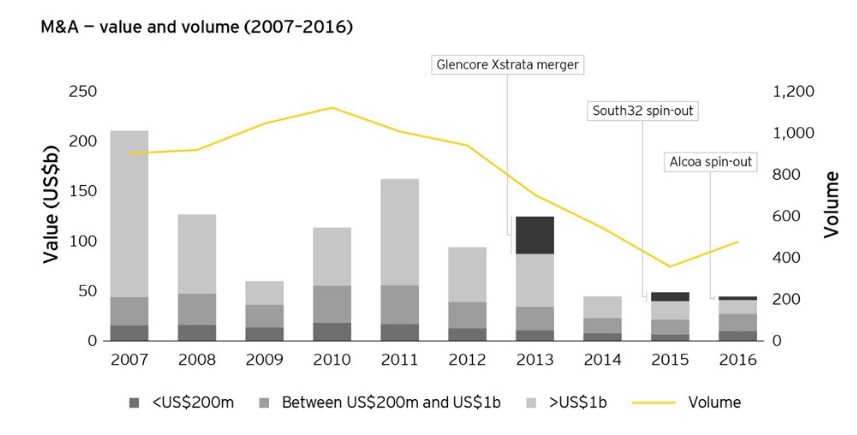

According to EY, the year on year value of mining M&A fell 9% in 2016 to $44.3 billion. While that sounds like a lot, it's the lowest level the industry has seen since 2004.

"Strategic restructuring and sovereign security drove some of the major deals through the choppy waters. This resulted in a marked increase in high-value transactions in the last quarter of the year, including the completion of Alcoa’s Arconic spin-off and FreeportMcMoRan’s sale of its Tenke Fungurume mine, which when combined had a deal value of US$6b, representing 14% of the total for the year," the report reads.

Who were the deal makers and what were they buying or selling? According to EY, China led all countries as both a target and an acquirer last year as a result of consolidation in its metal sector.

"The country more than doubled the value of domestic and cross-border acquisitions it made in 2016. 4 of the top 10 deals were undertaken by Chinese acquirers. China Molybdenum’s activities accounted for US$4.2b worth of acquisitions this year — just under 10% of the overall deal value in the sector — with the acquisition of Freeport’s Tenke Fungurume mine in DRC and Anglo-American’s niobium and phosphate assets in Brazil."

Copper was the commodity of most interest, comprising three of the top 10 deals, by value.

"This is reflective of longer term positive demand fundamentals for the commodity and a number of assets coming to market in the first half of the year that wouldn’t typically become available without the prevailing distress felt in the industry at the time. This provided an opportunity for strategic buyers, such as China Molybdenum and Sumitomo, to secure offtake from world-class assets."

However, the consultancy notes, the biggest jump was in aluminium deals, which rose from just US$244m in 2015 to US$3.4b in 2016. The largest one was Alcoa's $3.4b spin-off of its manufacturing business. "Aluminium, like steel, has been subjected to environmental crack-downs and cuts due to overcapacity in China, driving consolidation in the sector," notes EY.

It says deals in 2016 were overwhelmingly on the sell side, with divestments being the main driver behind the transactions in order for companies to restructure their portfolios and reduce debt.

Looking ahead to 2017, EY says the year is unlikely to see any of the mega, multi-billion-dollar deals seen during the supercycle, with the possible exception of consolidation among Chinese producers. The consultancy also hints that juniors might see some action towards year-end.

"Portfolio realignment and structural changes across certain industries, such as steel, coal and aluminium, will be the drivers of deal activities. The lack of exploration spend as a result of limited access to capital, will inevitably contribute to a future supply deficit and may trigger a return to financing across the juniors towards the end of 2017," according to the report.

Read the full report here. |

|