White House Candidates Set Divergent Trajectories for Energy, Commodity Sectors

By Maya Weber, Tom DiChristopher, Meghan Gordon, Jasmin Melvin, Tyler Godwin, Joniel Cha and Justine Coyne

October 10, 2020 - Stakes are high across the U.S. energy and commodities sectors as President Donald Trump and Democratic nominee Joe Biden vie to shape energy, climate and trade policy for the next four years.

Biden has called for a swift pivot to clean energy, while Trump has made the case for the country's abundant fossil fuel resources.

The winner will control regulations that could stymie or accelerate growth across energy sectors and markets, and help to direct investment. Trade policy also looms large in the election stakes — particularly for oil, natural gas, petrochemicals and metals — after Trump's trade policies have reshaped commodity flows.

Power Sector

Biden has proposed an aggressive plan to boost clean energy and reduce emissions to combat global warming, while Trump gives little attention to the issue in his "energy dominance" agenda emphasizing fossil fuel-fired generation.

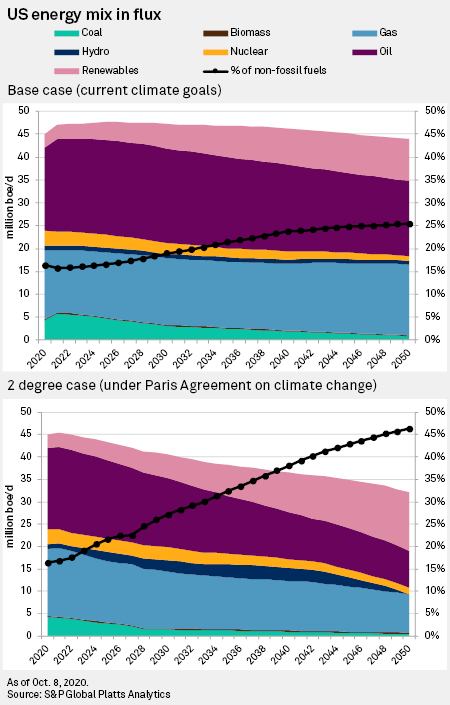

Under Biden, green energy developers could expand market share if climate impacts are heavily weighted. Biden's four-year, $2 trillion climate plan calls for carbon-free electricity by 2035 and makes infrastructure and clean energy investments core to an economic recovery package. Biden's position appears to make room for gas-fired generation but otherwise looks to accelerate retirements of fossil fuels.

Trump's agenda centers on regulatory rollbacks aimed at achieving energy independence. His backers credit first-term rollbacks with keeping energy prices low, and refraining from further regulations to speed retirement of low-cost coal plants. Trump's core priorities mention infrastructure improvements and bolstering cybersecurity defenses.

Nuclear Energy

Both candidates support existing and advanced nuclear reactors, as well as nuclear technology exports.

A Biden administration would create an Advanced Research Projects Agency on Climate within the U.S. Department of Energy to facilitate rapid commercialization of technologies such as advanced nuclear energy to attain net-zero electricity generation by 2035. A Biden administration would not, however, support uranium mining for environmental justice reasons.

The Trump administration has sought to revitalize the U.S. nuclear fuel cycle industry, including uranium production, conversion and enrichment, and to expand access to uranium deposits on federal lands.

Oil, Gas Production

The next presidential term will have a hand in energy policies as U.S. oil and gas producers attempt to recover from plunging prices and demand as a result of the coronavirus pandemic, all amid growing calls for an energy transition.

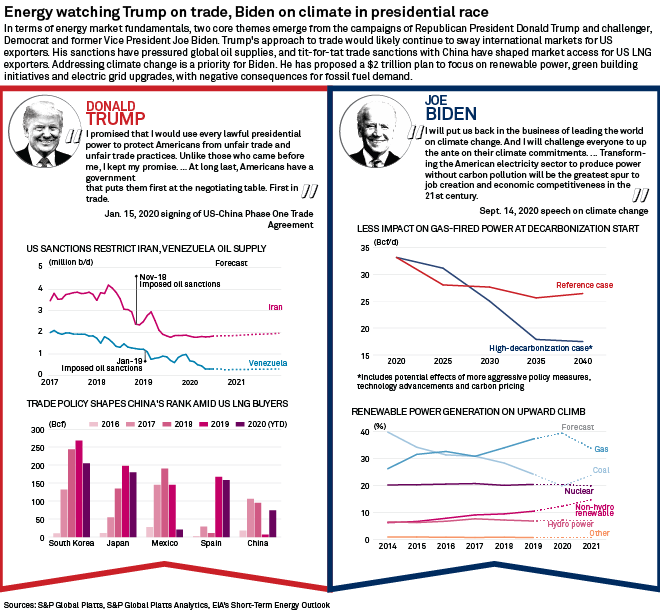

Biden has proposed halting new drilling permits on federal lands and waters, which puts 1.1 million b/d of oil output and 3.7 Bcf/d of gas output at risk by 2025 if existing permits and drilled-but-uncompleted wells are allowed to continue, according to Platts Analytics. A total federal drilling ban would cut oil output by 1.6 million b/d. Tighter emissions controls could also crowd out marginal producers. About 750,000 b/d and 9 Bcf/d of production in the U.S. comes from low-producing stripper wells, potentially more vulnerable to costs of increased regulations, according to Platts Analytics.

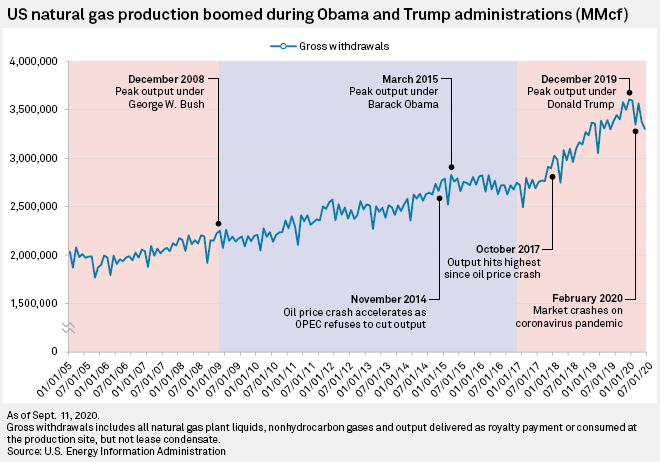

Trump would be expected to continue a deregulatory push started in his first term, although the oil and gas surge during this term was primarily a result of a 2015 end to crude export restrictions and the opening of several LNG export facilities.

Oil, Gas Infrastructure

Oil and gas pipelines already face relentless challenges from environmental litigation, but the 2020 election could add to hurdles.

Under Biden, a higher bar is likely for permitting of oil and gas infrastructure, with greater weight given to environmental impacts, including climate change. Some projects might be denied on those grounds, while others could still face post-authorization snags.

Trump has set policies aimed at streamlining permitting, although those have had mixed results. Prospects of a major build-out during a second term could be checked by the end of an oil and gas pipeline boom cycle, as well as fervent opposition and litigation from environmentalists and states.

LNG

Policies underlying LNG exports are unlikely to be upended under either election outcome, though trade policy remains a key unknown.

The Trump administration has promoted U.S. LNG and permitted additional terminals during this term, but only one has reached a final investment decision. While market forces played a major role, Trump's trade conflict with China also inhibited long-term contracts that support FIDs.

Biden has said little about LNG, but he has historically taken a holistic view of gas' role in U.S. policy, including its potential to displace coal in foreign markets and its role in diplomacy. A key question is whether Biden would begin unwinding the 25% tariffs chilling those contracts with buyers in China, a major growing market for LNG. Tighter methane regulation under Biden could add to production costs but help burnish gas' image as a clean resource, particularly as the U.S. seeks to market LNG in Europe and Asia.

Oil Sanctions

The next U.S. president's approach to OPEC producers Iran and Venezuela is the executive branch policy that could have the biggest global oil supply impact.

During Trump's term, U.S. sanctions on Iran and Venezuela cut oil supply by 3 million b/d and roiled shipping markets. Trump would be expected to keep enforcement tight, although Iran could try to test the waters for direct talks.

Biden would be expected to seek a quick return to the Iran nuclear deal, which could return 1.5 million b/d within a year. Biden is seen as more likely to grant Venezuela sanctions relief on humanitarian grounds.

Oil Trade

Under Trump, tensions with Beijing have flared to a degree that some analysts say could lead to a decoupling of U.S.-China ties, which could have significant trade impacts. China was seen as a top outlet for growing U.S. crude exports, but trade tensions have limited those flows, and China is not on track to meet its Phase 1 commitments for U.S. energy purchases.

While Biden is expected to tone down the rhetoric against China, analysts do not expect any major warming of ties that could lead to revived trade. "I think what Trump has done is put the spotlight on China," observed Chris Midgley, global head of analytics for S&P Global Platts. "I think everybody is now aligned that you need to take a far more direct approach with China, whereas before I think China had been just allowed to happily grow ... because everyone didn't want to aggravate the administration there. Now we will continue to see stronger, more aggressive trade negotiations."

Coal

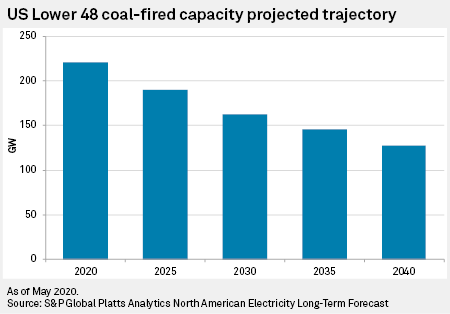

Coal's competitive position would be starkly challenged under either administration, although the election could determine whether strict regulations on mines and power plants are reinstated.

Trump promised to bring coal jobs back, and although coal sector employment increased to an average 53,150 in 2019 — up from 52,360 in 2016 — it was still down nearly 40% from 2008 levels, according to Mine Safety and Health Administration data. Mine employment fell to a record-low 41,724 in the second quarter due to market conditions amid the coronavirus pandemic. The administration lifted the moratorium on new federal coal leases in 2017 and rolled back several regulations on power plants and coal mines, but headwinds continue from low gas prices and utilities' efforts to green their portfolios.

Biden has said a new coal plant would not be built under his administration, but a large coal plant has not been built since 2013, and there currently are no plans for any new ones. According to S&P Global Market Intelligence data, nearly 85 GW of coal capacity was retired between 2008 and 2019, while another 25 GW is planned to be retired by 2025. Biden also could implement a moratorium on new coal leases on federal land, similar to an Obama-era ban. Over 40% of U.S. coal production, or about 303 million tons, was produced on federal land in 2019, according to U.S. Energy Information Administration data.

Metals

U.S. steelmakers expect bipartisan support for the industry to continue regardless of election outcome. However, a change in administration could bring revisions to tariffs on steel and aluminum under Section 232 of the Trade Expansion Act of 1962.

Since Trump implemented a 25% tariff on imported steel, U.S. steel import volumes have been on the decline. Following a 15% uptick in 2017, total U.S. steel imports fell roughly 12% year on year to 33.73 million tons in 2018, with imports accounting for 23% of the finished steel import market, according to the American Iron and Steel Institute. U.S. steel import volumes fell a further 17% in 2019 to 27.9 million tons, with imports accounting for 19% of the finished steel import market, according to the AISI.

Biden has committing to a review of the tariffs put in place by Trump in March 2018. He has also promised to enlist the U.S.'s international allies to collectively tackle unfair practices to ensure fair trade in steel, aluminum and other products.

Petrochemicals

The election outcome is significant for chemical producers in the U.S. and China because the trade war between the two countries has added costs for thousands of raw materials and products made with them.

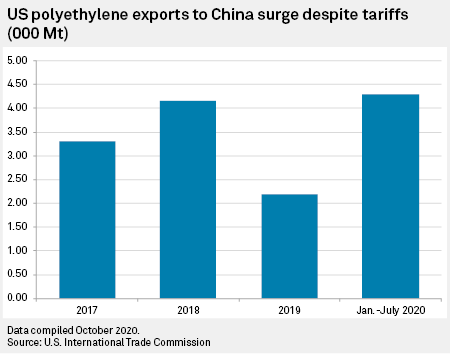

U.S. polyethylene exports to China fell 47% to 219,295 tonnes in 2019, the first full year of tariffs in effect, according to U.S. International Trade Commission data. The first seven months of 2020 saw those flows reach 428,843 tonnes, surpassing full-year flows in 2017 and 2018 and indicating U.S. export polyethylene pricing has been low enough to alleviate tariff concerns. Polyethylene is a resin used to make the world's most-used plastics, from grocery bags and shampoo bottles to buckets and milk jugs.

The U.S. has added 5.58 Mt/y of new PE capacity since 2017, with another 8 Mt/y slated to come through the 2020s. Most is targeted for export, and of that, China is the largest market. China's retaliatory tariffs target two types of PE that make up 91% of that new capacity.

Under Trump, most tariffs affecting petrochemical trade imposed in August 2018 remain in place at 25%. China's retaliatory tariffs largely target raw materials, including polyethylene.

Biden has called the trade war self-destructive, but that may not mean tariffs get lifted. Biden's campaign has said his administration would re-evaluate tariffs without committing to lifting them.

.gif)