|

Signature Sponsor

By Jon Gibbins, Director, UK CCS Research Centre, Professor of Power Plant Engineering, University of Sheffield; and Hannah Chalmers, Deputy Director (Network), UK CCS Research Centre, Senior Lecturer in Mechanical Engineering, University of Edinburgh

March 15, 2017 - At the Paris climate summit in December 2015, world leaders agreed to work to limit global climate change to 2°C and to try to achieve 1.5°C. To put the necessary cap on total cumulative greenhouse gas (GHG) emissions, leaders also agreed on net-zero emissions; that is, there must be “a balance between anthropogenic emissions by sources and removals by sinks of greenhouse gases in the second half of this century”.1

Net-zero emissions will require carbon capture and storage (CCS) for all fossil fuels and other technologies (e.g., biomass with CCS or direct air capture) for residual emissions from fossil fuel extraction and from other anthropogenic sources such as agriculture. This is radically different from the current position wherein CCS has been mainly identified with coal use and considered unnecessary for other fossil fuels. Coal-fired power generation with partial CCS is competing with unabated natural gas power plants—an impossible challenge economically unless gas and oil prices are very high. If, however, coal with CCS has to compete with gas with CCS then the situation is more balanced, particularly in markets such as China where the capital costs for coal power plants and coal prices are relatively low compared to natural gas.

Where It All Began: CCS and The Dash For Coal

Following earlier CCS initiatives such as the Sleipner injection project,2 the IEA GHG program,3 the Greenhouse Gas Technology conferences,4 the planning for CCS as part of the Gorgon LNG mega-project,5 and early SaskPower planning for coal CCS projects,6 CCS gained international prominence in the mid-2000s. Key events included the inaugural 2003 meeting of the Carbon Sequestration Leadership Forum (CSLF7) in the U.S., the 2005 Gleneagles Conference in Scotland,8 and the launch of the Global Carbon Capture and Storage Institute (GCCSI)9 in 2009.

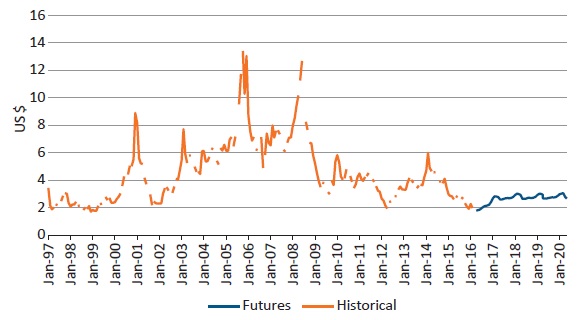

Subsequently, plans for CCS deployment expanded rapidly, driven by increasing demand and high natural gas and oil prices prior to the 2009 recession (see Figure 1) and continuing beyond 2009 because of commitments and established positions and, in the U.S., because of support for CCS in the so-called Stimulus Package (American Recovery and Reinvestment Act of 2009).

Figure 1. Historic and future North American natural gas market prices.

New CCS projects were expected to be placed on coal power plants, with major coal-build programs anticipated in the U.K., Europe, U.S., and Canada. Strong environmental protests were a driver for CCS on many of these proposed new coal-fired power plants. There was also an expectation that coal+CCS+EOR (enhanced oil recovery) would be competitive with natural gas with no CCS12 (e.g., SaskPower’s BD3 plant in Canada and the Petra Nova Project in Texas). However, the collapse of high natural gas and oil prices due to the recession resulted in a rethink of “peak oil”, and hence lower CO2 sales prices for EOR, and also of the need for a “dash for coal”.

Post-Recession Coal Blues in Countries Championing CCS

The current CCS position follows on from the changes after the recession and also from shale gas developments in North America. Minimal numbers of new coal plants have been built in CCS-championing countries (e.g., U.S., UK, Australia, Canada, and the Netherlands) with limited prospects for future construction. Electricity demand reduction is a partial reason for this in some markets (e.g., the UK) as is the growing output from intermittent, subsidized renewable generation sources. The Waxman-Markey climate legislation in the U.S., which contained incentives for CCS, failed to pass in the Senate in 2009, meaning coal+CCS+EOR in North America cannot compete with unabated natural gas, even with government capital support (such as from the U.S. stimulus incentives).

Without countries that champion CCS deploying it at scale, neither other developed economies (e.g., Germany, Poland) nor developing economies (e.g., China, India) are under much pressure to deploy CCS, even for coal—especially when there is no economic incentive or immediate global GHG emission reduction imperative to drive it.

CCS: A Technology for All Fossil Fuel Use

Alternative applications for CCS other than coal power exist and are recognized as vital in the long term by CCS-championing countries. However, there is currently no immediate GHG constraint nor public opinion driver to make CCS as imperative as it was for coal pre-recession. Globally important applications for meeting net-zero targets include:

Energy-intensive industries: usually grouped together, but in practice a heterogeneous range of applications (in terms of technology, scale, cost, location, etc.) and are almost always exposed to global competition. Therefore, production costs cannot be raised unilaterally by a country without import controls.

Natural gas CCS: limited new natural gas plants in many places, with construction under pressure from intermittent renewables; reluctance by some stakeholders to get CCS associated with natural gas power because it may then become effectively impossible to build; also U.S. Department of Energy (DOE) CCS funding is specifically for coal.

Biomass and waste combustion: of interest for negative emissions, but no developed proposals to incentivize negative emissions have been made anywhere yet.

Hydrogen: being discussed for heat in buildings, industry, and also, with interim storage, for electricity production in markets where (subsidized) zero-dispatch-cost renewables make CCS plant load factors uncertain.

The Immediate Way Ahead for CCS

The idea that CCS should be supported in ways analogous to renewables appears to be gaining traction in some countries, such as the UK (Feed in Tariffs with a Contract for Difference for electricity) and the U.S., but has received little attention elsewhere.

There are also some suggestions in the U.S. and UK that coal should be supported for political reasons, but coal+CCS would inevitably be more expensive than unabated gas. Coal+CCS versus natural gas+CCS would be more favorable to coal, but coal probably would still be more costly (particularly with large amounts of renewables in the system and hence uncertain load factors). The uncertainty in the timing and quantity for new nuclear power plants also makes the scope for CCS deployment and the strategic value of coal uncertain in the U.S. and UK.

CCS is therefore currently in a regrouping phase. Old plans either have almost all been completed or are defunct. New major projects and concepts for CCS are still nascent. This does not mean, however, that the CCS field should be inactive, rather the reverse. Major new projects take around a decade to develop and so work on them needs to be urgently advanced. The time available while this happens is a priceless resource that can be used to reduce costs and risks for the next tranche of major projects, as described below.

Making CCS Readiness More Widespread

The idea of building new fossil fuel infrastructure to be CCS ready is becoming more accepted in both developed and developing countries. Examples include the UK’s capture-ready guidelines used for power plant permitting and the Guangdong “CCS Ready Province” initiative in China. However, anecdotal evidence suggests that in some cases, where it is not a legal requirement, the fact that new facilities have been designed and located so as to be capture ready is deliberately not stated to avoid pressure to undertake CCS before competitors.

Establishing Proven CO2 Transport and Storage Infrastructure Options

Storage sites need to be further de-risked for prospective storage applications, with potentially significant costs, especially for offshore storage. Measures to make new plants CCS ready require some thought to be suitable for specific infrastructure and also to adapt to changes as CCS technology develops. Defining future shared pipeline routes (or CO2shipping options) would benefit CCS readiness plans greatly in some places.

Fast-track Small-Scale Projects

Successful small-scale projects (including on coal) could help to raise the profile of CCS and to partially rebuild industry confidence, and also could be used (in conjunction with other activities; see below) as part of a program of cost and risk reduction for future projects. Small-scale, modular CCS units could also have direct applications in some markets, not least for flexibility to cope with intermittent renewable outputs.

Raising Commercial Readiness of Post-combustion Capture

It seems unlikely that many (any?) new technology concepts will be brought to commercial readiness by the next stage of CCS deployment since this would require major speculative, funding for a reference plant. NET Power’s Allam Cycle is a possible exception. Recent large gasification-based pre-combustion capture trial plants (e.g., the Kemper plant in Mississippi) have not gone well. Post-combustion capture (PCC) projects, SaskPower and Petra Nova, are going largely as planned. When the next large-scale CCS projects are built, PCC may be the only commercially proven choice available for coal and gas power, and quite possibly the most competitive. PCC is also the only capture technology with full-scale experience available that can be used, with design studies and pilot-scale testing (see Figure 2), to produce improved second-generation PCC technologies for the next stage of CCS deployment.

Figure 2. Post-combustion test unit at the UK Carbon Capture and Storage Research Centre’s Pilot-scale Advanced Capture Facility (UKCCSRC PACT).

Developing CCS Policy, Regulations, Incentives, and Business Models

Ways to meet the cost of CCS need to be in place, as well as the organizations (private, possibly regulated, and/or public) with the necessary expertise and financial resources to undertake projects. National and international laws and regulations need to allow CCS. For example, the London Protocol amendments to allow cross-boundary transfer of CO2 for sub-seabed storage are not yet ratified. CCS treatment in GHG accounting may still have issues. Possible liability for stored CO2 is a potential show-stopper for private companies.

Acceptance of CCS as a Means of Delivering Clean Electricity Targets

Low-carbon electricity from fossil-fired power plants with CCS needs to be given equal treatment with nuclear and renewables in new policies to meet the Paris Agreement objectives. An example of this is the recent “Three Amigos” initiative by the U.S., Canada, and Mexico that includes producing 50% of electricity from clean sources. The calculation for the fraction of CCS plant output counted as zero carbon output needs to be rigorous environmentally, but it is essential that it is based on actual plant performance to encourage innovation in plant design and operation and to take advantage of the inherent flexibility of CCS for reducing costs.

CCS Uses in Energy-Intensive Industries

The cement, iron and steel, and chemicals industries are all major users of coal and other fossil fuels and are large GHG emitters in many countries. Effective utilization of the time between now and the beginning of the more widespread, commercially driven deployment of large-scale CCS facilities can be based on fast-tracked small-scale work as well as larger industrial projects where CO2 storage or EOR markets are already available (e.g., the Decatur Project, Shell Canada’s Quest Project, Air Products’ Port Arthur project).

CCS Training and Opportunities For Work in the CCS Industry

One important challenge in establishing and rolling out CCS as a global option for reducing CO2 emissions is ensuring sufficient numbers of trained people are available at all stages of the project life cycle. Particularly for early projects, it is likely that most contributors to project design and delivery (and supporting policy and regulation) will be applying skills normally used for other applications.

A range of initiatives are underway to develop and support a cohort of CCS professionals. For example, most universities with CCS research interests include course material on CCS in their undergraduate and MSc programs. Several MSc programs are dedicated to CCS and PhD-level programs with significant CCS content are also available. Some graduates from such programs are developing careers in CCS R&D and consultancy, while others are using the skills developed during their studies in other energy-related roles.

It is important to ensure that individuals who are early in their career are able to gain as much practical experience as possible and also to learn from more experienced practitioners who may retire before widespread deployment of CCS. In this context, “learning by doing” at pilot-scale facilities (see Figure 3) and through targeted international collaboration is particularly important in the next decade as part of a broader effort to ensure that necessary expertise is grown to facilitate effective global rollout of CCS in the longer term.

Figure 3. Early-career researchers and CCS specialists at the CCPilot100+ final meeting. Six complementary R&D projects and 23 four-week secondments were provided to research students on the CCPilot100+ pilot post-combustion capture unit at Ferrybridge Power Station in West Yorkshire, England.

CCS projects are operating in many countries, but prospective workers and researchers should look at a variety of scales and different fuels and applications. The range of disciplines required is growing, with specialists in areas other than CCS becoming more important as technologies are deployed at pilot scale or larger in “real” applications, and a range of new issues are discovered and addressed. Strong cooperation between industry and researchers is also needed for cost reduction. It may appear that there are not many job opportunities now, but CCS worker numbers will have to grow rapidly if net-zero emissions are to be achieved. With exponential growth in CCS deployment during the next two or three decades, experienced workers in all aspects of CCS development, design, and construction will be in short supply. Once a significant number of CCS installations are in place a large workforce of operators will be required. Experience with power plants and other long-lived major infrastructure investments also suggests that in-service modifications, improvements, and maintenance will be a continuous and major business.

The drive to achieve net-zero emissions from all fossil fuel use within perhaps 50 years or less will be a challenging but vital job for the current generation, and many future generations, of CCS workers and researchers. |

|