.gif)

|

Signature Sponsor

By David Fickling

June 13, 2017 - Is Glencore Plc's last-minute bid for Rio Tinto Group's Australian thermal coal assets about quantity, or quality? It's a bit of both.

With a tenement footprint that's more or less surrounded by Glencore's own mines, Rio Tinto's Hunter Valley pits have long been an obvious target for the trader.

In volume terms, the $2.55 billion offer looks like the sort of deal that typically went down a decade ago, when the thermal coal used in power stations was a hot commodity and the likes of Rio Tinto and Anglo American Plc were looking to add assets, rather than exit ones still on their books.

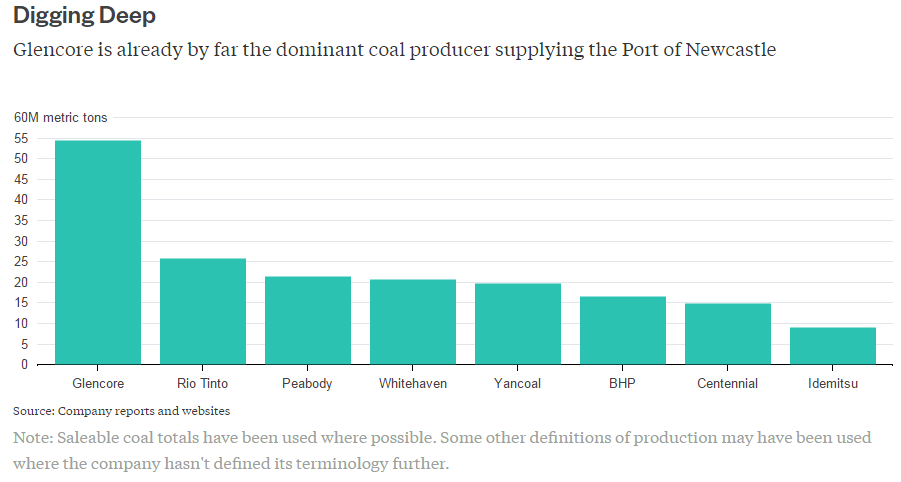

Glencore is by far the biggest coal miner in Australia's Hunter Valley, the region north of Sydney that supplies the world's biggest coal export harbor at Newcastle. But its mines are rapidly depleting, and will run out in about a decade at current production rates. Add Rio Tinto's vast resource base and lower output pace, and you could comfortably extend that deadline into the mid-2030s or beyond.

Hang on, though. Won't the world have stopped burning coal by the mid-2030s? Well, not quite. While coal is in a long-term decline, even the more aggressive decarbonization scenarios examined by the Intergovernmental Panel on Climate Change see it providing 10 percent to 14 percent of the world's primary energy by 2050 -- well down from about 30 percent at present, but still enough to represent a significant lump of carbon.

That's the real kicker in Glencore's bid. As the company demonstrated in its announcement, buying Rio Tinto's mines will allow Glencore to link up a jigsaw puzzle of pits scattered across the upper Hunter Valley.

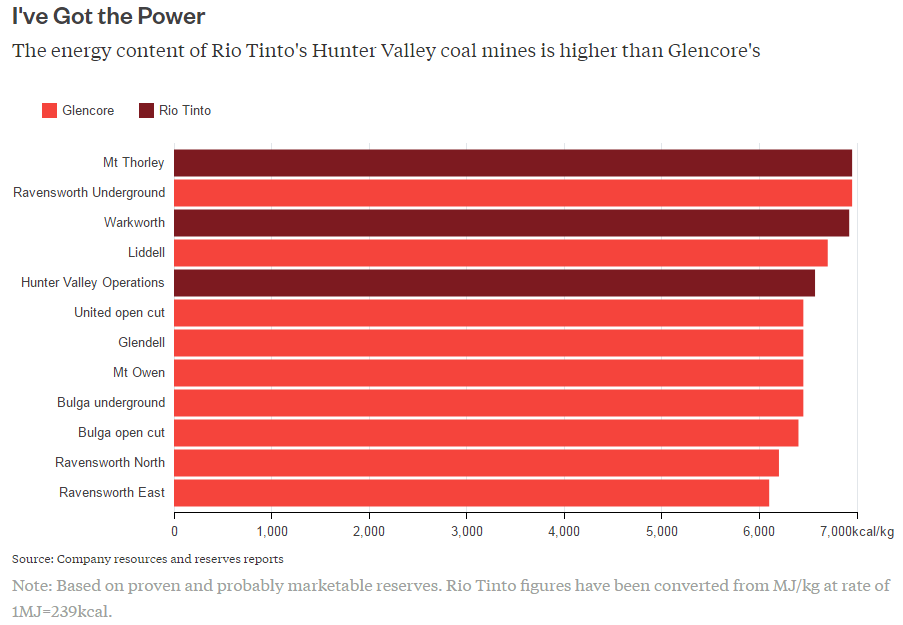

That will yield opportunities to shift tonnage between mines and blend some of its coals with Rio Tinto's, to create an overall higher-quality product.

The gap between 6,100 kilocalories per kilogram at Glencore's Ravensworth East mine and 6,950kcal/kg at Rio Tinto's Mt Thorley may seem insignificant, but far smaller distinctions can have a dramatic effect on pricing: 6,000kcal/kg coal at Newcastle port typically sells for about 24 percent more than 5,500kcal/kg product, according to Gadfly's calculations. Geology tends to be destiny for miners, so opportunities to upgrade coal quality in this way are rare.

Whether Glencore's Chief Executive Officer Ivan Glasenberg gets his wish is another matter. There's already another bidder in the queue, in the form of Yancoal Australia Ltd., the local subsidiary of China's Yanzhou Coal Mining Co., which agreed to purchase the mines for $2.45 billion back in January.

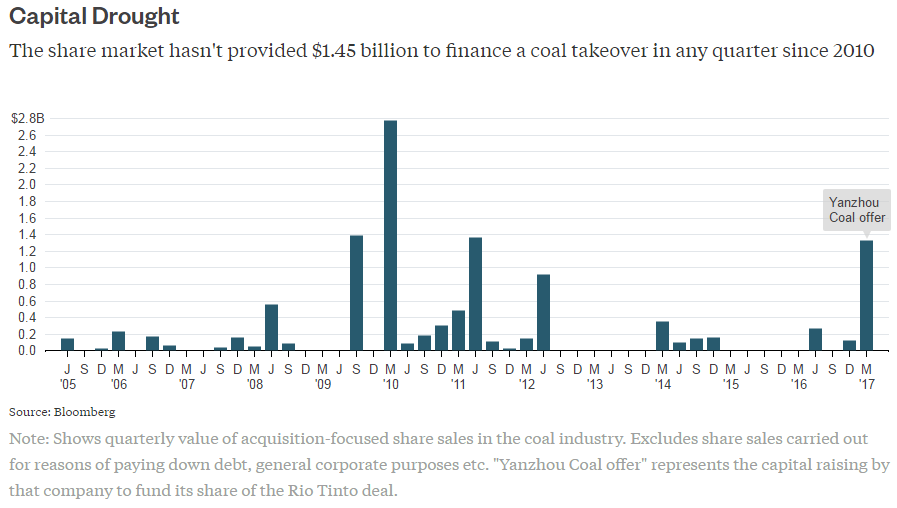

Glencore is making such a low-ball offer -- just $100 million more than Yancoal -- because it doubts its rival will be able to raise the cash. Yancoal Australia's market cap is just $293 million, so it plans to get the money by selling new shares. Its 78 percent dominant shareholder, Yanzhou Coal, will provide only $1.03 billion, and the second-largest shareholder, Noble Group Ltd., is probably more likely to reduce than add to its 13 percent position, given its own pronounced cash difficulties.

That means the bulk of the remaining $1.42 billion will have to come from new investors -- but shareholders haven't shown that sort of enthusiasm for coal acquisitions since 2010.

Hence the attractions of Glencore's offer, which isn't subject to the availability of finance.

Pity Rio Tinto's Chief Executive Officer Jean-Sebastien Jacques. With Yancoal still saying that it will be able to raise the funding, he must decide before Glencore's June 26 deadline whether to risk offending China Inc. by picking the greater certainty offered by the Anglo-Swiss company, or to risk the deal falling over altogether by going with Yancoal.

Mining bosses weighing multi-billion dollar bidding wars for their assets should normally be expected to be in a happy position. In this instance, Jacques looks like an exception. |

|