|

Signature Sponsor

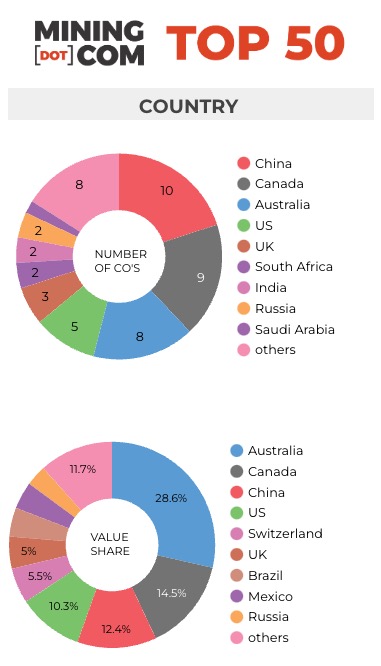

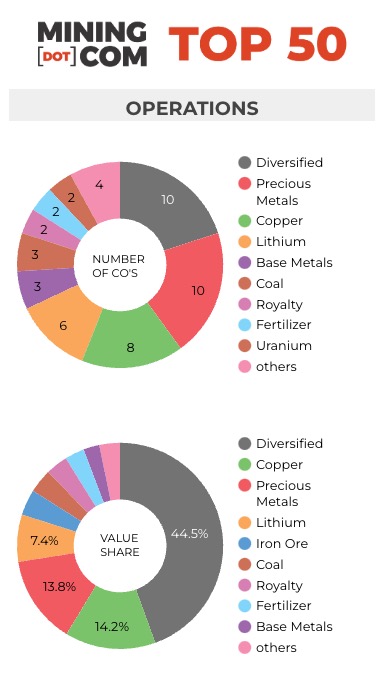

July 23, 2023 - MINING.COM’s ranking of world’s biggest miners welcomes the first Indonesian company to the top tier and Perth as the city hosting the greatest number on the list. At the end of the first quarter of 2022 metals and minerals were setting all-time records led by bellwether copper which briefly traded above $5 a pound or more than $11,000 per tonne. Iron ore, the second most traded bulk commodity after crude oil and the cash cow for the top tier of the mining world, was above $150 a tonne. Both commodities are down by more than 20% since then – officially a bear market. At the end of Q1 2022, the MINING.COM TOP 50* ranking of the world’s biggest miners hit an all time record of a collective $1.75 trillion. Half way through 2023 and mining valuations have slumped a total of $356 billion after giving up a collective $47 billion during the second quarter. The Top 50 now has a combined market value of $1.38 trillion – back to levels seen end-June 2021. Indonesian debutThe first Indonesian company to make it into the top 50 is Amman Minerals Internasional, owner and operator of the Batu Hijau copper and gold mine and developer of the adjacent Elang project. Elang is one of the world’s largest undeveloped copper and gold porphyry deposits and is currently in the feasibility stage. Indonesia has become a red-hot IPO market this year and Amman was the largest of the year so far. The company debuted in Jakarta on July 7, raising more than $700m, and enters the ranking at no 46 with a valuation just shy of $9 billion or 135 trillion rupiah, up smartly since the IPO. Harita Nickel, which listed in Jakarta in April raising $672m, has had a tough go of it and the stock has shed more than 30% since then as nickel prices decline at a similar rate. In USD terms Harita Nickel is worth less than $4 billion which places the stock outside the 70 most valuable mining stocks globally. Lithium ranks growLithium producer Pilbara Minerals makes a spectacular entry into the Top 50 at position no 42 after spending several quarters bubbling under the ranking.  Pilbara Minerals shares are up over 40% so far this year, lifting its value to over $10 billion, surpassing that of fellow lithium miner and Perth neighbour, Mineral Resources. Pilbara Minerals, which is the ranking’s best performer for the quarter, brings the number of companies based in the Western Australia capital to five, surpassing the tally of Vancouver, BC as the top home base. Another Perth-based lithium miner, IGO, has been climbing the charts and currently sits at number 52 in the ranking at a valuation just shy of $8 billion. Worth a collective $101 billion, lithium stocks make up 7.4% of the value of the Top 50. The strength of the lithium sector outside China has been remarkable given the precipitous decline in prices for the battery metal since hitting all time highs in November last year. Official projections from top producer Australia, responsible for half the world’s output of lithium, are for more pain over the next three years amid a production boom. The disappointing launch this week of lithium futures in Guangzhou China is another harbinger of weakness and points to further losses for shares in Ganfeng and Tianqi, already down 50% over the past 12 months.  Potash problemsFertiliser prices have been on a dramatic decline over the last year and after hitting 14-year highs in April last year on the back of the Ukraine war and potash at the port of Vancouver has now halved in value. Stock of sector heavyweights Nutrien, which cut its guidance and production at one of its Saskatchewan mines this month due to a port strike, and Mosaic have fallen sharply as a result, with the North American companies losing a combined $10 billion during the quarter. The retreat in the market cap of fertilizer maker ICL Group in Tel Aviv sees the company drop out of the Top 50 altogether. While Russian potash is finding itself onto world markets, deliveries from Belarus remain below the pre-war total. At the same time large new projects are being developed including in Brazil, the world’s foremost importer of the crop nutrient, and in Canada, where the province of Manitoba greenlit a new potash mine and processing plant in June. The Canadian government earlier this year injected $75 million into BHP’s Jansen project as the Anglo-Australian giant seeks to fast-track construction of the mine which if built to full capacity will be the world’s largest.  *NOTES: Source: MINING.COM, Mining Intelligence, Morningstar, GoogleFinance, company reports. Trading data from primary-listed exchange at July 17, 2023 where applicable, currency cross-rates July 18, 2023. Percentage change based on US$ market cap difference, not share price change in local currency. As with any ranking, criteria for inclusion are contentious. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information. That, of course, excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining, which owns the world’s largest gold mine, Eurochem, a major potash firm, and a number of entities in China and developing countries around the world. Another central criterion was the depth of involvement in the industry before an enterprise can rightfully be called a mining company. For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or warrant a seat on the board? This is a common structure in Asia and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec. Levels of operational or strategic involvement and size of shareholding were other central considerations. Do streaming and royalty companies that receive metals from mining operations without shareholding qualify or are they just specialised financing vehicles? We included Franco Nevada, Royal Gold and Wheaton Precious Metals on the basis of their deep involvement in the industry. Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy where power, ports and railways make up a large portion of revenues pose a problem as does battery makers like CATL which is increasingly moving upstream, but where mining still make up a small portion of its valuation. Another consideration is diversified companies such as Anglo American with separately listed majority-owned subsidiaries. We’ve included Angloplat in the ranking but excluded Kumba Iron Ore in which Anglo has a 70% stake to avoid double counting. Similarly we excluded Hindustan Zinc which is listed separately but majority owned by Vedanta. Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel, Adani Enterprises and many others. Head office refers to operational headquarters wherever applicable, for example BHP and Rio Tinto are shown as Melbourne, Australia, but Antofagasta is the exception that proves the rule. We consider the company’s HQ to be in London, where it has been listed since the late 1800s. Please let us know of any errors, omissions, deletions or additions to the ranking or suggest a different methodology. |

|