|

Signature Sponsor

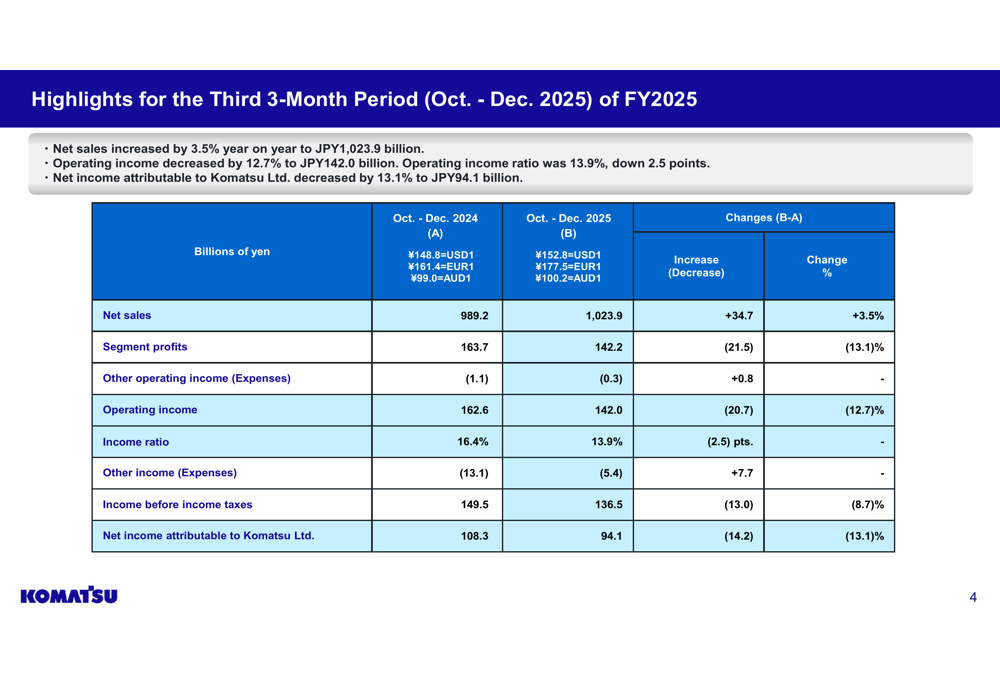

February 3, 2026 - Komatsu Ltd. (TYO:6301) released its third-quarter fiscal year 2025 results on January 30, 2026, revealing a mixed performance characterized by sales growth but declining profits. The construction and mining equipment manufacturer’s stock responded positively to the results, rising 4.79% to close at ¥6,213, as the company’s performance exceeded analyst expectations despite operational challenges. The results come amid a complex global economic environment for heavy equipment manufacturers, with regional variations in demand and ongoing supply chain pressures affecting the industry. Komatsu’s ability to grow revenue despite these headwinds demonstrates the company’s market resilience, though profit margins have come under pressure. Quarterly Performance HighlightsFor the three months ended December 31, 2025 (Q3 FY2025), Komatsu reported net sales of ¥1,023.9 billion, representing a 3.5% increase year-on-year. However, operating income declined by 12.7% to ¥142.0 billion, resulting in an operating income ratio of 13.9%. Net income attributable to Komatsu Ltd. decreased by 13.1% to ¥94.1 billion. As shown in the following quarterly highlights chart:

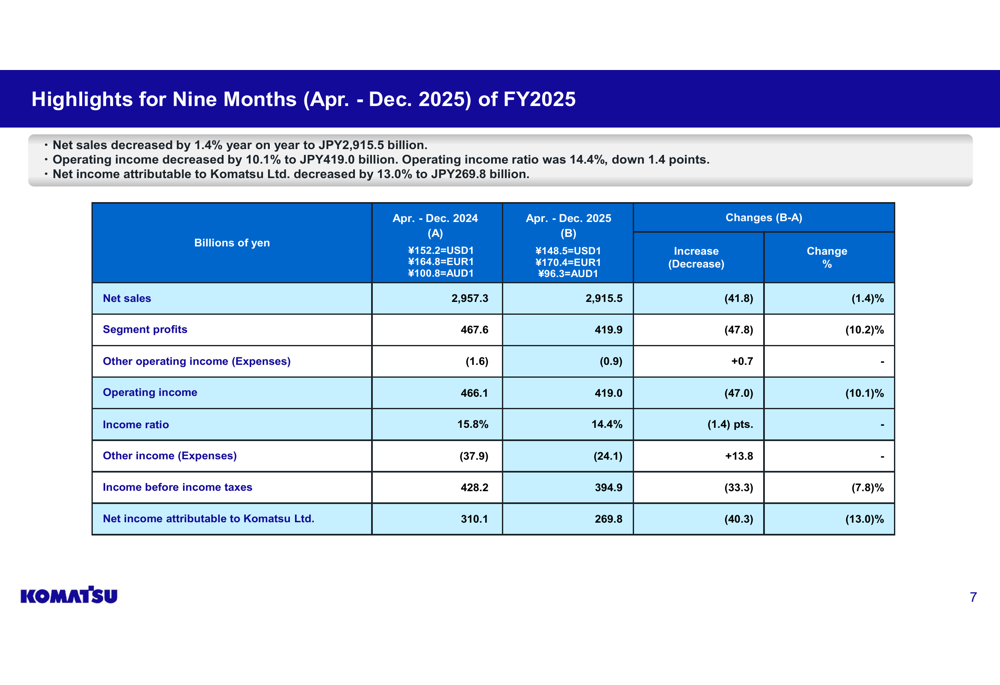

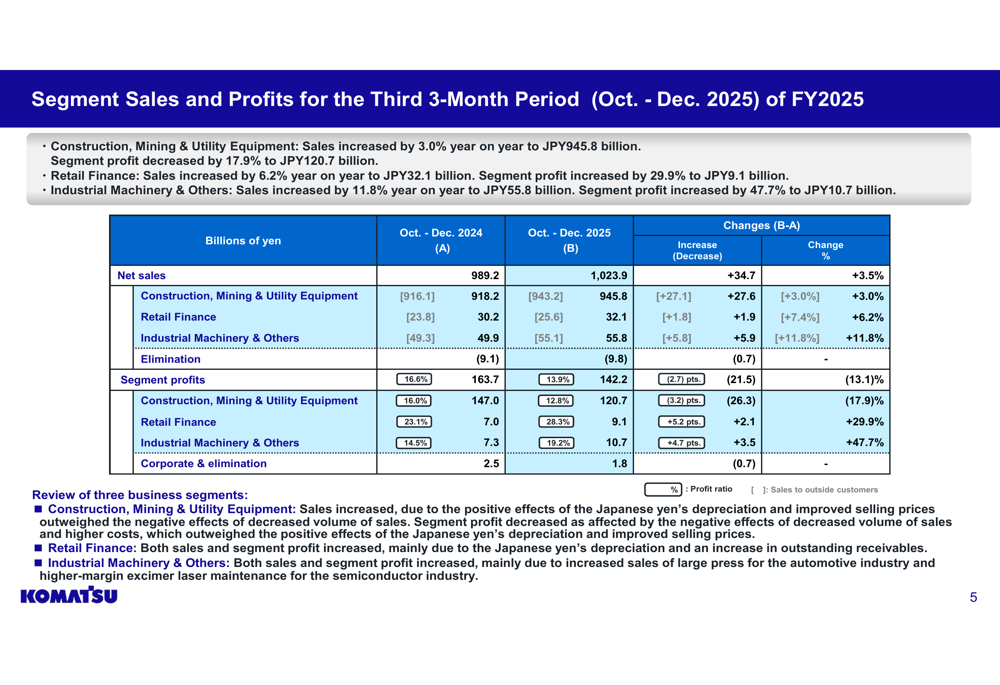

The company’s earnings per share reached ¥104.02, surpassing the forecast of ¥96.41 by 7.89%, according to market data. This positive surprise helped drive investor confidence despite the profit decline, as it demonstrated Komatsu’s ability to outperform expectations in a challenging environment. For the nine-month period (April-December 2025), the company’s performance showed similar trends with net sales decreasing by 1.4% year-on-year to ¥2,915.5 billion and operating income declining by 10.1% to ¥419.0 billion. The nine-month operating income ratio stood at 14.4%, while net income attributable to Komatsu Ltd. decreased by 13.0% to ¥269.8 billion. The following chart illustrates the nine-month performance metrics: Segment AnalysisKomatsu’s business segments showed divergent performance in Q3 FY2025. The core Construction, Mining & Utility Equipment segment, which accounts for the majority of the company’s business, saw sales increase by 3.0% year-on-year to ¥945.8 billion. However, segment profit decreased significantly by 17.9% to ¥120.7 billion, indicating substantial margin pressure. In contrast, the Retail Finance segment demonstrated strong profit growth with sales increasing by 6.2% to ¥32.1 billion and segment profit rising by 29.9% to ¥9.1 billion. The Industrial Machinery & Others segment was the standout performer, with sales increasing by 11.8% to ¥55.8 billion and segment profit surging by 47.7% to ¥10.7 billion. The segment breakdown for Q3 is illustrated in the following chart:

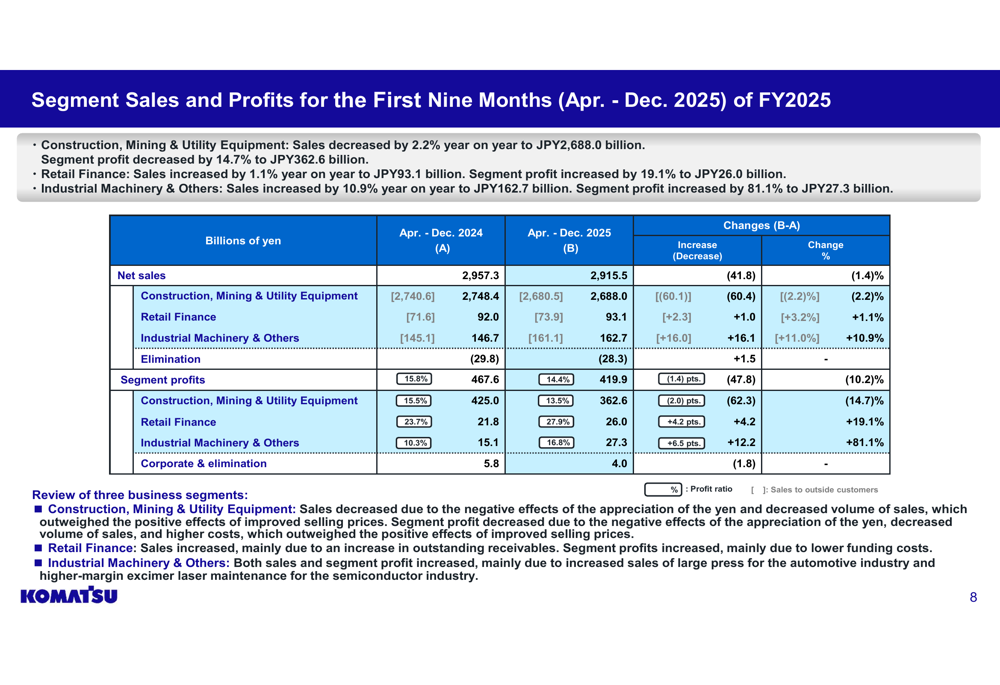

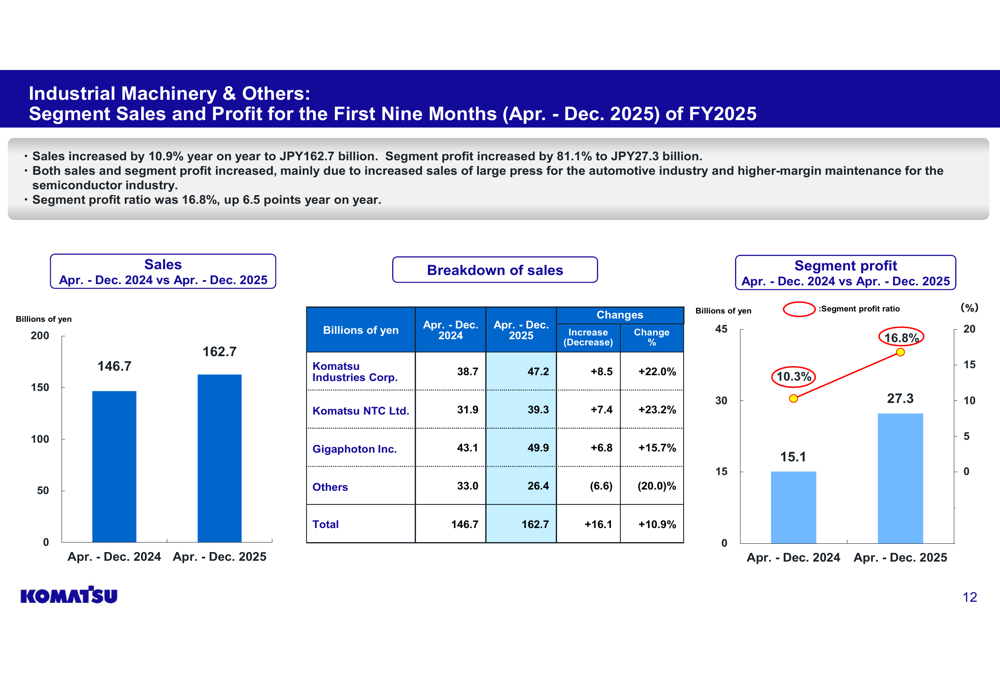

For the nine-month period, the Construction, Mining & Utility Equipment segment experienced a 2.2% decrease in sales to ¥2,688.0 billion, with segment profit declining by 14.7% to ¥362.6 billion. The Retail Finance segment showed a modest 1.1% increase in sales to ¥93.1 billion, but segment profit grew significantly by 19.1% to ¥26.0 billion. The Industrial Machinery & Others segment continued its strong performance with sales increasing by 10.9% to ¥162.7 billion and segment profit surging by 81.1% to ¥27.3 billion. The nine-month segment performance is detailed in this chart:

The Industrial Machinery segment’s exceptional performance was attributed to increased sales of large presses for the automotive industry and higher-margin maintenance services for the semiconductor industry, resulting in a segment profit ratio of 16.8%.

Similarly, the Retail Finance segment showed improved profitability with assets increasing by ¥148.0 billion and new contracts rising by ¥32.5 billion. The segment’s return on assets (ROA) improved from 2.1% in December 2024 to 2.3% in December 2025. To see the full presentation, click here (PDF).

|

|